Blank Promissory Note for a Car Template

Blank Promissory Note for a Car Template

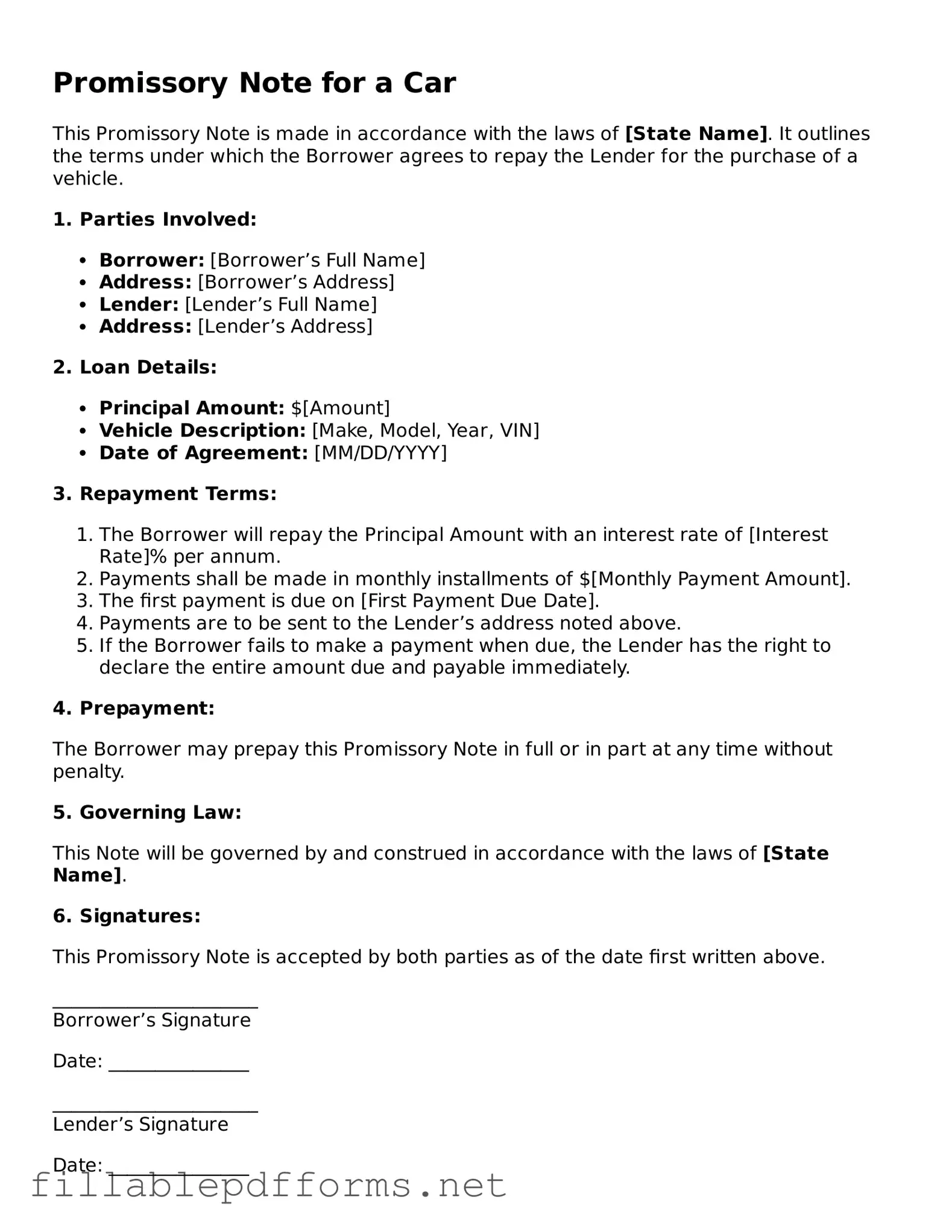

When purchasing a car, especially through a private sale or a financing agreement, a Promissory Note for a Car can be an essential document. This form outlines the borrower's promise to repay the lender for the vehicle's purchase price, detailing the terms of the loan. It typically includes important information such as the amount borrowed, the interest rate, the repayment schedule, and any consequences for late payments or defaults. The note serves as a legal record of the transaction, protecting both the buyer and the seller. By clearly stating the obligations of each party, it helps prevent misunderstandings down the road. Additionally, the Promissory Note can specify whether the loan is secured by the car itself, which means the lender can reclaim the vehicle if payments are not made. Understanding this form is crucial for anyone entering into a car financing agreement, as it lays the groundwork for a smooth transaction and fosters trust between the parties involved.

Incorrect Borrower Information: Many people fail to provide accurate personal details such as their full name, address, or Social Security number. This can lead to issues with loan processing and potential legal complications.

Missing Loan Amount: Some individuals forget to clearly state the total amount being borrowed. This can create confusion and disputes later on regarding the terms of repayment.

Omitting Interest Rate: It’s crucial to specify the interest rate. Without this, the terms of the loan may be unclear, leading to misunderstandings about how much will be owed over time.

Failure to Include Payment Schedule: Not detailing when payments are due can result in missed payments. A clear schedule helps both parties understand their obligations.

Neglecting Signatures: Some forget to sign the document or have the lender sign as well. A promissory note is not valid without the appropriate signatures, which can nullify the agreement.

Not Reading the Fine Print: Individuals often skip over the terms and conditions. Understanding all clauses is essential to avoid surprises or misunderstandings in the future.

When it comes to the Promissory Note for a Car, many people hold misconceptions that can lead to confusion or mistakes. Understanding the truth behind these beliefs is essential for anyone considering financing a vehicle. Here’s a list of common misconceptions:

Understanding these misconceptions helps clarify the role of a promissory note in car transactions. It’s always best to approach any financial agreement with clear knowledge and the right documentation.

After obtaining the Promissory Note for a Car form, you will need to fill it out carefully. This document will outline the terms of the loan for purchasing the vehicle. Ensuring accuracy and clarity in your entries is essential, as this will help prevent any misunderstandings later on.

Once the form is completed, review it to ensure all information is correct. Both parties should keep a copy for their records. If necessary, consult with a legal professional for any clarifications or additional steps.

When filling out the Promissory Note for a Car form, it’s essential to get it right. Here are some things you should and shouldn't do:

Release of Promissory Note - This form is used to officially release a promissory note from its obligations.

When engaging in financial transactions, having a clear understanding of the terms is essential. Utilizing a New Jersey Promissory Note form can greatly facilitate this process, as it provides a comprehensive outline of the repayment terms, including the interest rate and schedule. For those interested in drafting such an agreement, the Promissory Note form serves as a valuable resource, ensuring that both parties are protected and informed throughout the lending process.

When dealing with a Promissory Note for a Car, understanding the key elements can help ensure a smooth transaction. Here are some important takeaways to keep in mind:

By following these guidelines, you can create a comprehensive Promissory Note that protects both the lender and the borrower throughout the car financing process.