Blank Promissory Note Template

Blank Promissory Note Template

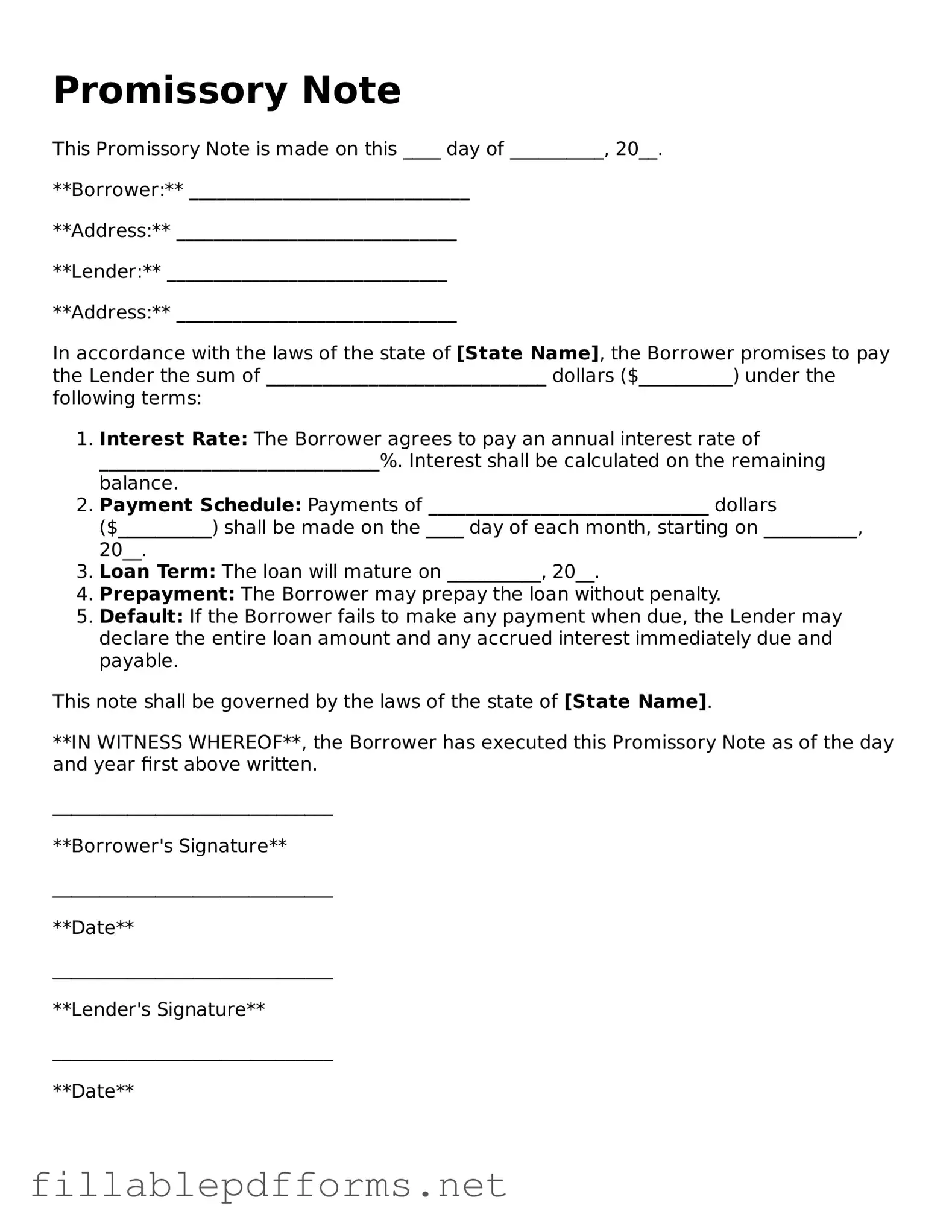

When engaging in a financial transaction, clarity and security are paramount. The Promissory Note form serves as a crucial tool in this regard, outlining the terms of a loan agreement between a borrower and a lender. It typically includes essential details such as the principal amount, interest rate, payment schedule, and maturity date. This form not only specifies the obligations of the borrower but also protects the lender's interests. In addition to these fundamental elements, a Promissory Note may also address what happens in the event of default, providing guidelines for resolution. The simplicity and straightforwardness of this document make it accessible for individuals and businesses alike, ensuring that both parties understand their rights and responsibilities. Understanding the nuances of a Promissory Note can help prevent misunderstandings and foster trust in financial relationships.

Inaccurate Borrower Information: Failing to provide the correct name, address, or contact details of the borrower can lead to confusion and potential legal issues.

Missing Lender Information: Just as with the borrower, omitting the lender's details can complicate the enforcement of the note.

Unclear Loan Amount: Not specifying the exact amount being borrowed can create disputes. It's crucial to state the sum clearly.

Vague Interest Rate: Including an ambiguous interest rate or leaving it blank can result in misunderstandings about repayment terms.

Failure to State Repayment Terms: Not outlining how and when the loan will be repaid can lead to complications down the line.

Omitting Signatures: A promissory note is not valid without the signatures of both parties. Neglecting this step renders the document unenforceable.

Ignoring Date of Agreement: Failing to date the document can cause issues regarding the timeline of the loan.

Neglecting to Include Default Terms: Not specifying what happens in the event of default can leave both parties unprotected.

Using Ambiguous Language: Employing vague terms can lead to different interpretations. Clarity is essential in legal documents.

Not Keeping Copies: Failing to retain a copy of the signed note for personal records can complicate future reference or disputes.

Understanding the Promissory Note form is essential for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are five common misconceptions:

Clarifying these misconceptions can help individuals navigate their financial agreements more effectively.

After you have obtained the Promissory Note form, it is important to fill it out accurately to ensure that all parties involved understand the terms of the agreement. Once completed, the form will need to be signed and dated by both the borrower and the lender. This step is crucial for the document to be legally binding.

When filling out a Promissory Note form, it is important to follow specific guidelines to ensure accuracy and legality. Here are ten things to keep in mind:

How to Write a Letter of Recommendation for Citizenship - A way to express love and commitment in official paperwork.

For those looking to access important tax information, the Sample Tax Return Transcript form serves as a valuable resource, offering a comprehensive summary of an individual's federal income tax return for a specific year. This official document encapsulates essential details such as income, adjustments, tax calculations, and payments made, all of which provide taxpayers and authorized parties with a clear picture of their financial situation. To learn more about obtaining this form, you can visit My PDF Forms, which offers further guidance on the process.

Affidavit of Support - It protects immigrants from becoming a public burden.

When dealing with a Promissory Note, it is essential to understand its structure and purpose. Here are key takeaways regarding the completion and utilization of this financial document: