Profit And Loss PDF Template

Profit And Loss PDF Template

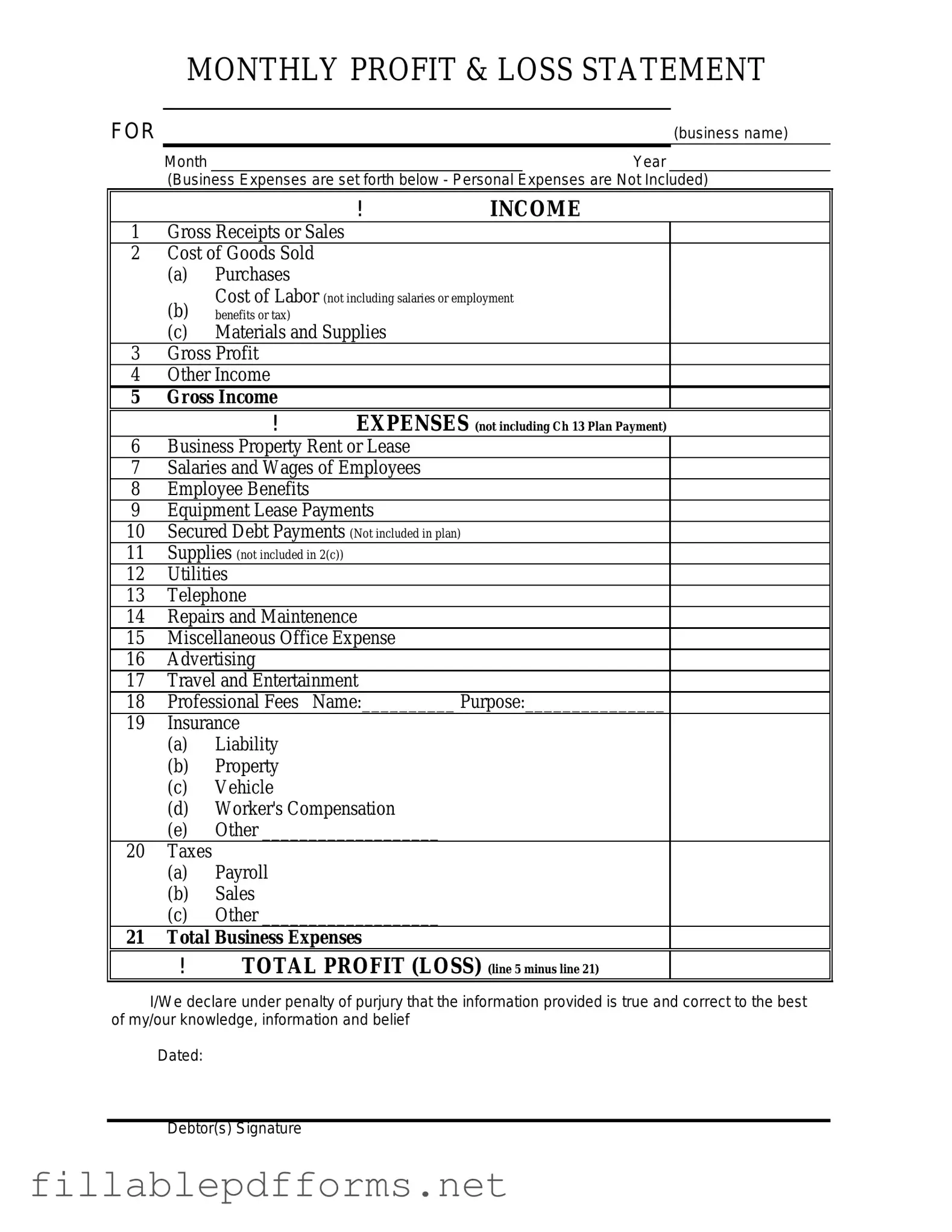

The Profit and Loss form is a crucial financial document that provides a snapshot of a business's financial performance over a specific period. It summarizes revenues, costs, and expenses, allowing stakeholders to assess profitability and operational efficiency. By detailing income generated from sales and services, the form highlights how effectively a company converts its resources into profit. Additionally, it outlines various expenses, including direct costs associated with production and overheads, which are essential for understanding the overall financial health. This document serves not only as a tool for internal management but also as a vital resource for investors, creditors, and tax authorities. A well-prepared Profit and Loss form can reveal trends, inform strategic decisions, and guide future budgeting efforts, making it an indispensable part of any business's financial toolkit.

When filling out the Profit and Loss form, it’s important to be careful and thorough. Here are six common mistakes people often make:

Missing Income Entries: Some individuals forget to include all sources of income. This can lead to an inaccurate representation of financial health.

Incorrect Categorization of Expenses: Misclassifying expenses can distort profit calculations. Ensure that each expense is placed in the correct category.

Omitting Non-Operating Income: Failing to report income from investments or other non-business activities can result in an incomplete picture of overall earnings.

Not Updating for Seasonal Variations: Some businesses experience seasonal fluctuations. Ignoring these can misrepresent profitability during certain periods.

Using Estimates Instead of Actual Figures: Relying on estimates rather than actual numbers can lead to inaccuracies. Always use verified data when possible.

Neglecting to Review for Errors: Skipping a final review can allow mistakes to go unnoticed. A thorough check can catch errors before submission.

By avoiding these mistakes, you can ensure that your Profit and Loss form accurately reflects your financial situation.

Here are some common misconceptions about the Profit and Loss form:

Completing the Profit and Loss form is essential for understanding your financial performance over a specific period. This process involves gathering relevant financial data and accurately inputting it into the designated fields. Follow the steps below to ensure a thorough and precise completion of the form.

When filling out the Profit and Loss form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are six things you should and shouldn't do:

Aia Qualification Statement - Providing accurate and complete information on the A305 is essential for contractor reliability.

For individuals looking to understand the transfer process, the New Jersey ATV Bill of Sale is a vital document that serves as a formal record. It is important to familiarize yourself with the necessary details, making it beneficial to explore resources available for a complete guide to learning about the ATV Bill of Sale form. You can find more information at your guide to the New Jersey ATV Bill of Sale.

Texas Driver License Renewal Form - The DL-43 form may require a signature to validate the application.

Filling out and using the Profit and Loss form is essential for understanding your business's financial health. Here are key takeaways to consider: