Attorney-Verified Promissory Note Form for North Carolina State

Attorney-Verified Promissory Note Form for North Carolina State

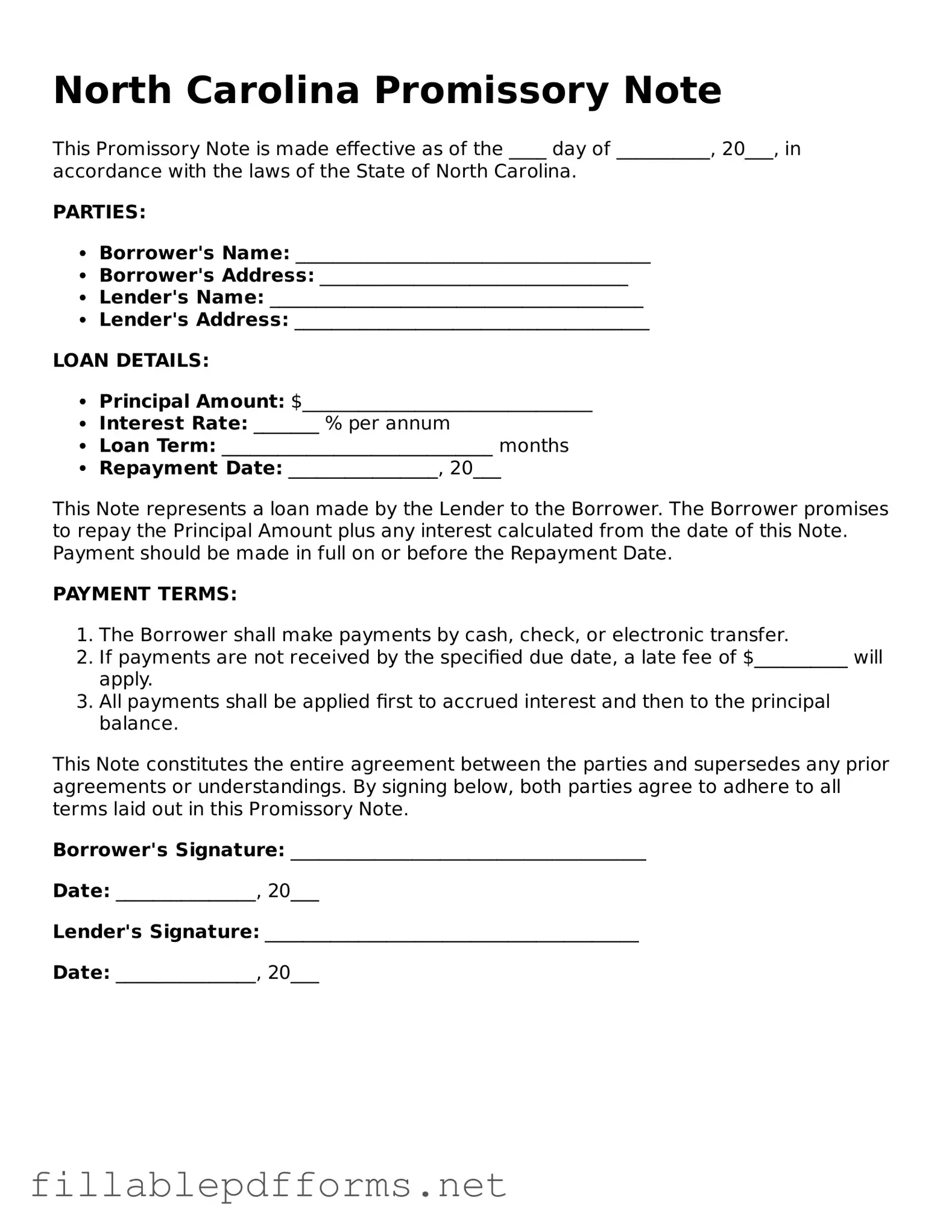

The North Carolina Promissory Note form serves as a crucial financial instrument for individuals and businesses engaging in lending and borrowing transactions. This legally binding document outlines the terms of a loan, including the principal amount, interest rate, repayment schedule, and any applicable fees. It establishes the borrower's commitment to repay the loan within a specified timeframe, while also detailing the lender's rights in the event of default. The form typically includes spaces for both parties to provide their names, addresses, and signatures, ensuring that the agreement is personalized and enforceable. Furthermore, it may incorporate clauses addressing prepayment options and late payment penalties, thereby offering clarity and protection for both the lender and the borrower. By adhering to the requirements set forth by North Carolina law, this Promissory Note form not only facilitates transparent financial transactions but also fosters trust between parties, ensuring that all aspects of the loan agreement are clearly articulated and understood.

Not Including All Necessary Information: One common mistake is failing to provide complete details. Borrowers should ensure that their names, addresses, and the loan amount are all accurately filled in. Missing any of this information can lead to confusion later.

Incorrect Loan Amount: Sometimes, individuals miscalculate the loan amount or simply write the wrong number. It’s crucial to double-check this figure to avoid disputes in the future.

Omitting Payment Terms: Clearly outlining the payment terms is essential. People often forget to specify how and when payments should be made, which can lead to misunderstandings between the borrower and lender.

Ignoring Interest Rates: If the loan involves interest, it must be stated explicitly. Some individuals neglect to include this information, which can create issues regarding repayment expectations.

Not Signing the Document: A promissory note is not valid without signatures. Many forget to sign the form or assume that a verbal agreement is sufficient. Without signatures, the document lacks legal weight.

Failing to Date the Note: It’s important to include the date when the note is signed. This date marks the beginning of the loan agreement and can impact repayment schedules.

Not Keeping Copies: After filling out the form, people often neglect to keep copies for their records. Having a copy is vital for both parties to refer back to in case of any disputes or questions.

When it comes to financial agreements, understanding the nuances of a promissory note is crucial. In North Carolina, several misconceptions often arise about the promissory note form. Here’s a breakdown of some common misunderstandings.

Understanding these misconceptions can help individuals and businesses navigate the world of promissory notes more effectively. It’s always a good idea to consult with a professional if you have questions or need assistance with creating or enforcing a promissory note.

After obtaining the North Carolina Promissory Note form, you will need to complete it accurately to ensure it serves its intended purpose. Follow the steps below to fill out the form correctly.

When filling out the North Carolina Promissory Note form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do:

By following these guidelines, you can help ensure that your Promissory Note is filled out correctly and effectively. Attention to detail is key in legal documents.

Texas Promissory Note Requirements - Parties involved in the note may include individuals, organizations, or financial institutions.

Washington Promissory Note - Borrowers can use promissory notes to consolidate debt or finance major purchases.

Promissory Note for Loan - Promissory notes help establish lender-borrower relationships.

When engaging in a vehicle transaction, it is vital to utilize the appropriate documentation to ensure a smooth ownership transfer. The Florida Motor Vehicle Bill of Sale form is essential for this process, providing crucial details about the sale. For those looking to acquire this form, it can be accessed online at https://floridaformspdf.com/printable-motor-vehicle-bill-of-sale-form, allowing both buyers and sellers to complete their transactions with confidence.

Promissory Notes for Personal Loans - Both parties should date the document accurately to reflect the initiation of the agreement.

When filling out and using the North Carolina Promissory Note form, consider the following key takeaways: