Attorney-Verified Promissory Note Form for New York State

Attorney-Verified Promissory Note Form for New York State

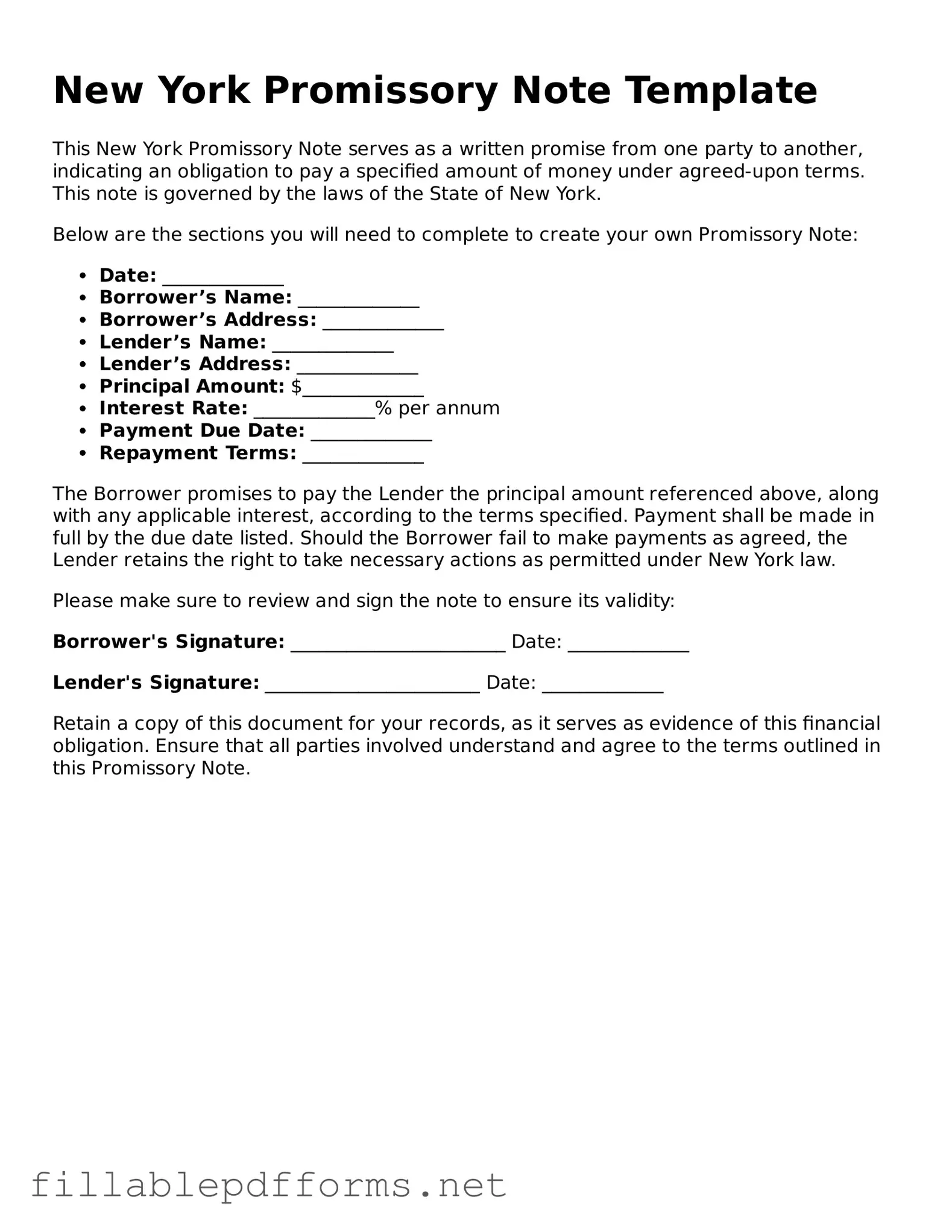

In the bustling financial landscape of New York, a Promissory Note serves as a crucial instrument for both borrowers and lenders. This legally binding document outlines the terms of a loan agreement, specifying the amount borrowed, the interest rate, and the repayment schedule. Understanding the key components of the New York Promissory Note form is essential for anyone looking to engage in lending or borrowing money. The document typically includes details such as the names and addresses of both parties, the maturity date, and any collateral that may secure the loan. Additionally, it may outline the consequences of default, ensuring that both parties are aware of their rights and obligations. By grasping these elements, individuals can navigate their financial agreements with confidence and clarity, minimizing potential disputes and fostering trust in their transactions.

Incorrect Names: Failing to use the full legal names of all parties involved can lead to confusion or disputes later.

Missing Signatures: Not signing the document is a common oversight. All parties must sign for the note to be valid.

Ambiguous Terms: Using vague language when describing the loan terms can create misunderstandings. Clarity is essential.

Omitting Dates: Forgetting to include the date of the agreement can complicate enforcement or record-keeping.

Wrong Amount: Entering an incorrect loan amount can lead to disputes. Double-check the figures before finalizing.

Interest Rate Errors: Miscalculating or misrepresenting the interest rate can result in legal issues. Ensure accuracy in this section.

Failure to Specify Payment Terms: Not clearly outlining the payment schedule can create confusion regarding when payments are due.

Ignoring State Laws: Not adhering to New York state regulations regarding promissory notes can invalidate the document.

Not Keeping Copies: Failing to retain copies of the signed note can lead to complications if disputes arise in the future.

Inadequate Witnessing or Notarization: Depending on the situation, not having the document witnessed or notarized may affect its enforceability.

When it comes to the New York Promissory Note form, several misconceptions often arise. These misunderstandings can lead to confusion for both lenders and borrowers. Here are four common misconceptions:

Understanding these misconceptions can help individuals navigate the complexities of financial agreements more effectively. Clarity and communication are key to ensuring that both parties feel secure in their commitments.

Completing the New York Promissory Note form requires careful attention to detail. Once you have the form in front of you, you will need to provide specific information to ensure it is valid and enforceable. Follow these steps to fill out the form accurately.

After completing the form, both parties should keep a copy for their records. This ensures that each party has access to the agreed-upon terms. If necessary, consider having the document notarized for additional legal protection.

When filling out the New York Promissory Note form, there are several important guidelines to keep in mind. Adhering to these can help ensure that the document is clear and enforceable.

Promissory Note for Loan - They can serve different purposes, from personal loans to mortgages.

Texas Promissory Note Requirements - Sometimes, a payment schedule is included to outline repayment timelines.

To facilitate the transaction, it is advisable to use a reliable source for the Bill of Sale document, such as My PDF Forms, which can provide a template that meets all necessary legal requirements and ensures clarity for both the buyer and seller.

Promissory Note Template Ohio - This document acts as proof of the loan agreement and can provide clarity in financial dealings.

When filling out and using the New York Promissory Note form, several important considerations come into play. Here are key takeaways to keep in mind:

By following these guidelines, individuals can effectively navigate the process of creating and utilizing a New York Promissory Note.