Attorney-Verified Loan Agreement Form for New York State

Attorney-Verified Loan Agreement Form for New York State

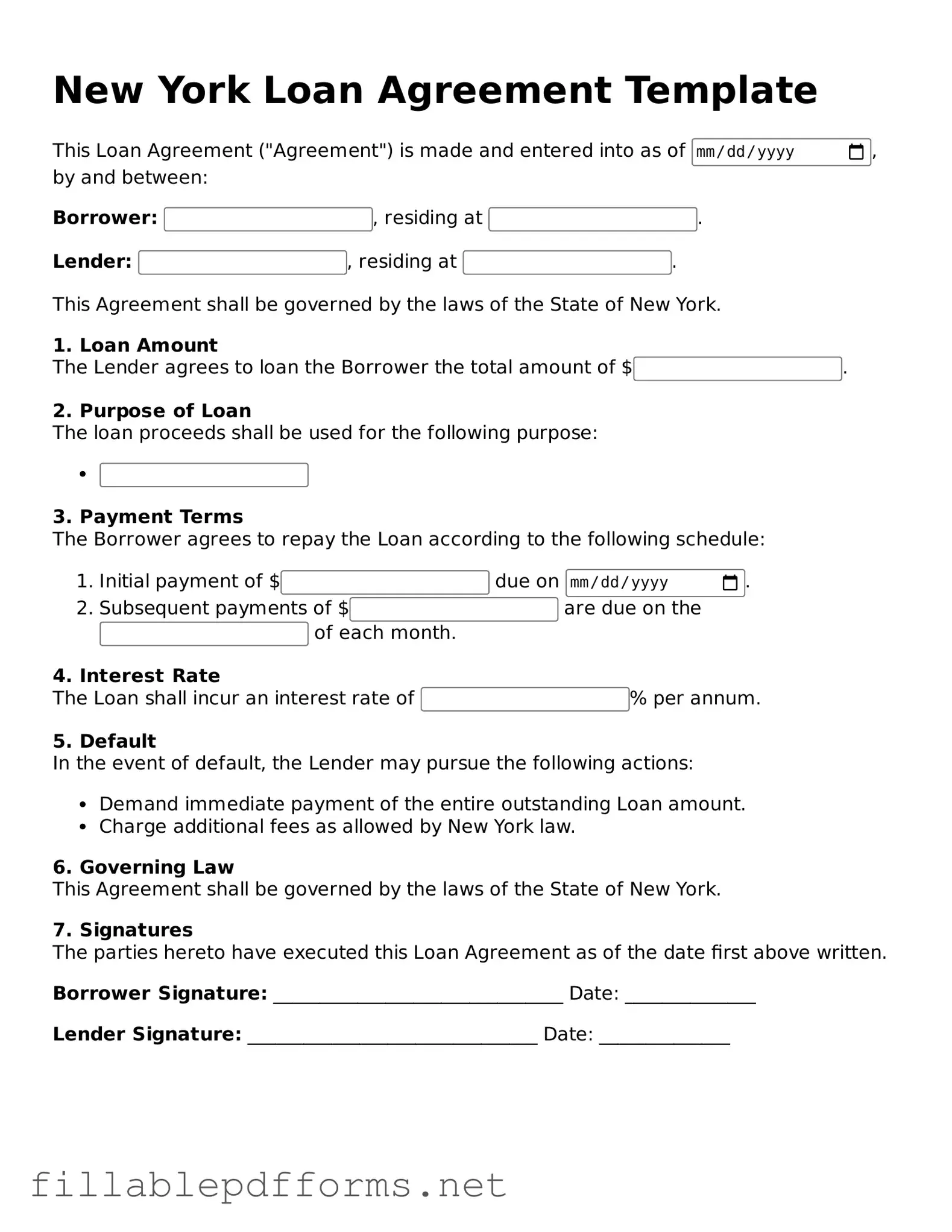

The New York Loan Agreement form is a crucial document for anyone entering into a lending arrangement in New York. This form outlines the terms and conditions of the loan, ensuring that both the lender and borrower have a clear understanding of their obligations. Key aspects include the loan amount, interest rate, repayment schedule, and any fees associated with the loan. Additionally, the form specifies the consequences of default, providing a framework for resolving disputes. By detailing the rights and responsibilities of each party, the New York Loan Agreement helps protect both the lender’s investment and the borrower’s interests. Understanding this form is essential for anyone looking to secure a loan in New York, as it lays the groundwork for a successful financial transaction.

Failing to provide accurate personal information. Borrowers sometimes enter incorrect names, addresses, or contact details, which can lead to processing delays.

Omitting financial information. Some individuals do not include all necessary financial details, such as income or existing debts, which can affect loan approval.

Not reading the terms and conditions. Many people overlook the fine print, which may contain important clauses about interest rates and repayment terms.

Using outdated information. Applicants may submit forms with old employment or financial data, which can misrepresent their current situation.

Neglecting to sign the document. It is common for individuals to forget to sign the agreement, rendering it invalid.

Incorrectly calculating the loan amount. Some borrowers miscalculate how much they need, leading to either insufficient funds or excessive borrowing.

Not providing required documentation. Missing documents, such as proof of income or identification, can delay the loan process.

Ignoring deadlines. Failing to submit the form by the required date can result in lost opportunities or unfavorable loan terms.

The New York Loan Agreement form is often misunderstood. Below are seven common misconceptions, along with clarifications for each.

This is not true. The New York Loan Agreement can be used for loans of any size, whether small or large. It is designed to provide a clear framework for both lenders and borrowers.

In reality, the Loan Agreement can be used for both personal and commercial loans. It serves as a versatile tool for various lending situations.

Each Loan Agreement can be customized to fit the specific terms and conditions agreed upon by the parties involved. This flexibility allows for tailored agreements that meet individual needs.

Signing the Loan Agreement does not guarantee that the loan will be funded. Approval is contingent upon various factors, including creditworthiness and compliance with lender policies.

While the Loan Agreement is binding, parties can negotiate amendments if both agree to the changes. It is important to document any modifications in writing.

In many cases, notarization is not required. However, having the agreement notarized can add an extra layer of authenticity and may be necessary for certain types of loans.

This is incorrect. The Loan Agreement remains important even after the loan has been repaid. It serves as a record of the transaction and can be referenced if disputes arise in the future.

Completing the New York Loan Agreement form is a critical step in securing a loan. It is essential to provide accurate information to ensure a smooth process. Follow the steps below to fill out the form correctly and efficiently.

After filling out the form, review it carefully to ensure all information is accurate. Submitting the completed form promptly will help facilitate the loan process. Be prepared for any follow-up questions or additional documentation that may be required.

When filling out the New York Loan Agreement form, attention to detail is crucial. Here’s a helpful list of things to do and avoid:

Texas Promissory Note Form - Small print in the agreement may contain essential details, so read carefully.

In addition to understanding the importance of the New York Mobile Home Bill of Sale, it is advisable for both parties to access reliable resources to facilitate the transaction process. For an easy and efficient way to obtain this document, you can visit My PDF Forms, which provides the necessary forms needed for a smooth ownership transfer.

When filling out and using the New York Loan Agreement form, it is crucial to pay attention to several important details. Here are key takeaways to consider:

Taking these steps can help ensure that both parties are protected and that the loan process goes smoothly.