Attorney-Verified Deed in Lieu of Foreclosure Form for New York State

Attorney-Verified Deed in Lieu of Foreclosure Form for New York State

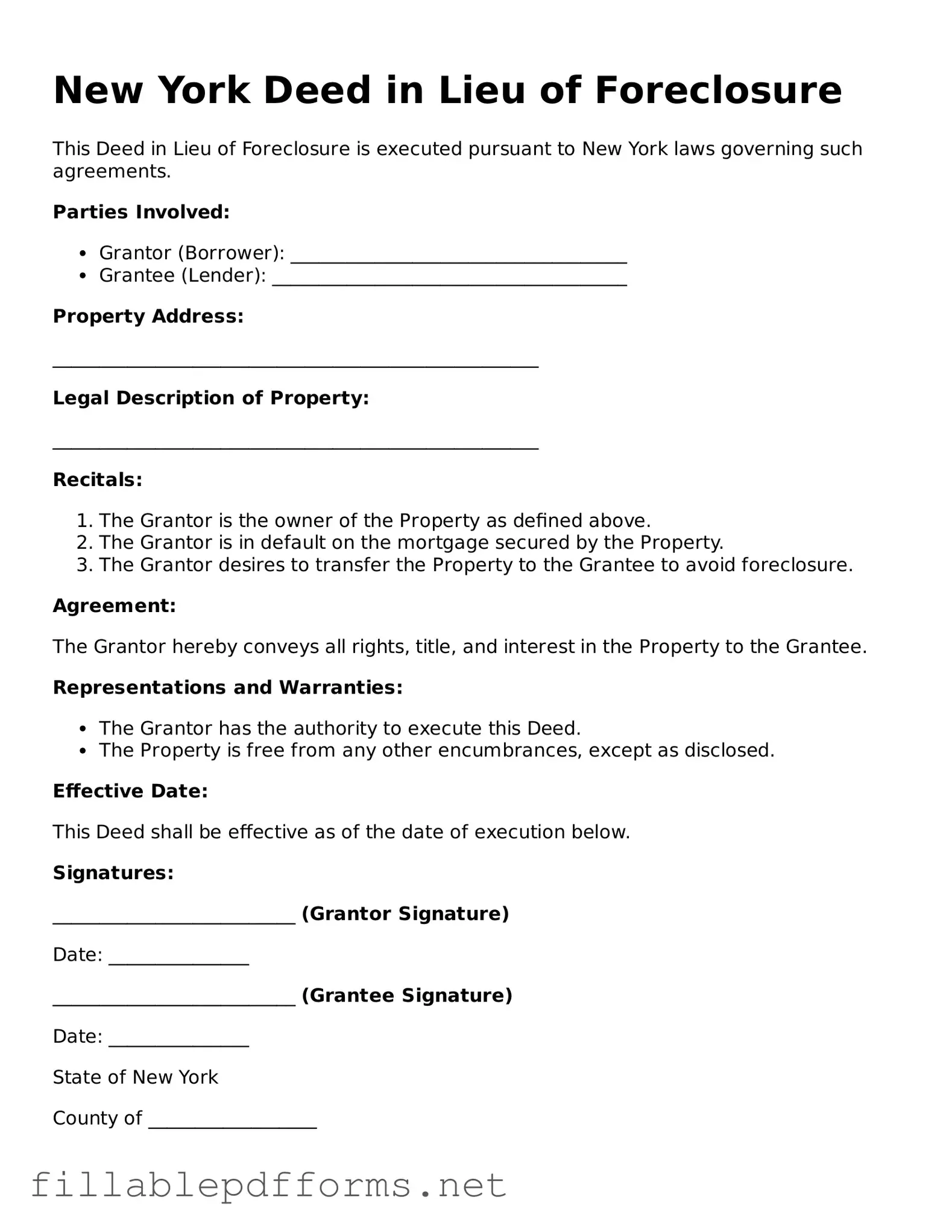

The Deed in Lieu of Foreclosure form is an important legal instrument in New York, designed to provide a more amicable resolution for homeowners facing financial difficulties. This form allows property owners to voluntarily transfer the title of their property back to the lender, effectively avoiding the lengthy and often stressful foreclosure process. By doing so, homeowners can mitigate the negative impact on their credit scores and move forward with their lives more quickly. The form typically includes essential details such as the names of the parties involved, a description of the property, and any relevant financial obligations. Additionally, it may outline the conditions under which the deed is executed, ensuring both parties understand their rights and responsibilities. This process can be beneficial for lenders as well, as it reduces the costs associated with foreclosure proceedings and allows them to take possession of the property without extensive legal battles. Understanding the nuances of the Deed in Lieu of Foreclosure form can empower homeowners to make informed decisions during challenging financial times.

Failing to provide accurate property information. Ensure that the property address, legal description, and tax identification number are correct.

Not including all necessary parties. All individuals or entities listed on the mortgage must sign the deed.

Overlooking the requirement for notarization. The deed must be signed in the presence of a notary public to be legally binding.

Ignoring local laws and regulations. Each county may have specific requirements for the deed. Research these before submission.

Neglecting to consult with a legal professional. Legal advice can help avoid costly mistakes and ensure compliance with all laws.

Submitting the form without reviewing it thoroughly. Double-check for errors or omissions that could delay the process.

Failing to understand tax implications. A deed in lieu of foreclosure may have tax consequences that should be considered.

Not communicating with the lender. Keeping an open line of communication can clarify expectations and requirements throughout the process.

When dealing with a Deed in Lieu of Foreclosure in New York, many people hold misconceptions that can lead to confusion and poor decision-making. Here are seven common myths about this legal process, along with clarifications to help you understand it better.

This is not entirely true. While it does allow homeowners to avoid foreclosure, it can still impact your credit score significantly. Additionally, you may not be completely free from debt, as lenders might pursue deficiency judgments in some cases.

A Deed in Lieu of Foreclosure is different from a short sale. In a short sale, the home is sold for less than the mortgage amount with the lender's approval, while in a Deed in Lieu, the homeowner transfers ownership of the property directly to the lender.

This misconception is misleading. Homeowners can initiate this process even before foreclosure proceedings begin, as long as they are experiencing financial hardship.

Not all lenders have the same policies. Some may not accept a Deed in Lieu of Foreclosure, especially if there are junior liens on the property. Always check with your lender for their specific requirements.

This is incorrect. A Deed in Lieu of Foreclosure does not involve any cash payment to the homeowner. Instead, the homeowner relinquishes their property to the lender to settle the mortgage debt.

While it may seem straightforward, the process can be lengthy and involves negotiations with the lender. It often requires documentation and can take time to finalize.

This is not always the case. Depending on the state laws and specific circumstances, homeowners may still owe money if the property is worth less than the mortgage balance.

Understanding these misconceptions is crucial for homeowners considering their options. Always consult with a qualified professional to explore the best path forward in your unique situation.

After completing the New York Deed in Lieu of Foreclosure form, you will need to submit it to the appropriate authorities. This typically involves filing it with the county clerk's office where the property is located. Make sure to keep copies for your records.

When filling out the New York Deed in Lieu of Foreclosure form, it's essential to approach the process with care. Here are seven important dos and don’ts to consider:

What Does an Arizona Homeowner Lose When Choosing to Use Deed in Lieu of Foreclosure? - Homeowners must ensure they understand all stipulations before signing the deed.

In addition to its importance in defining roles and responsibilities, the New York Operating Agreement form can also enhance the credibility of your LLC by clearly setting out the operational framework. For those looking to streamline the process of creating this essential document, resources like My PDF Forms can be incredibly helpful in ensuring that all necessary components are covered effectively.

Deed in Lieu of Foreclosure Ohio - This form is often viewed positively by lenders as it minimizes legal costs associated with foreclosure.

When dealing with the New York Deed in Lieu of Foreclosure form, consider the following key takeaways: