Attorney-Verified Promissory Note Form for New Jersey State

Attorney-Verified Promissory Note Form for New Jersey State

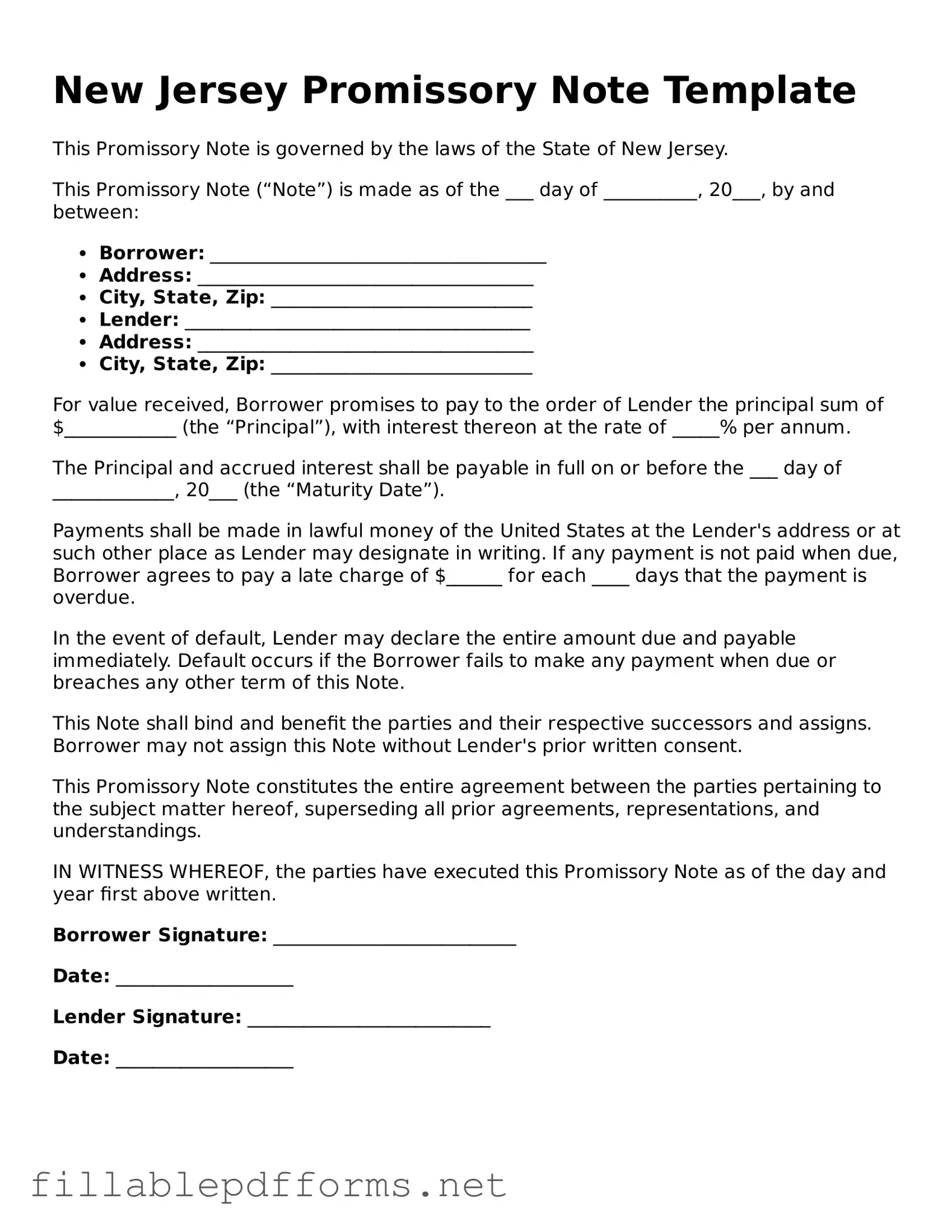

The New Jersey Promissory Note form serves as a crucial document in various financial transactions, allowing individuals or businesses to formalize a loan agreement. This form outlines the terms under which one party agrees to pay a specific amount of money to another party, establishing clear expectations for repayment. Key aspects include the principal amount, interest rate, payment schedule, and any applicable fees. Furthermore, the document typically specifies the consequences of default, ensuring that both the lender and borrower understand their rights and obligations. By using this standardized form, parties can avoid misunderstandings and create a legally binding agreement that protects their interests. Whether you are lending money to a friend or entering into a business arrangement, understanding the components of the New Jersey Promissory Note is essential for a smooth transaction.

Failing to include the date at the top of the form. This is crucial as it establishes when the agreement takes effect.

Not clearly identifying the borrower and lender. Full names and addresses should be provided to avoid confusion.

Leaving out the loan amount. Ensure that the amount is written in both numbers and words for clarity.

Neglecting to specify the interest rate. This detail is essential for understanding the total repayment obligation.

Not indicating the payment schedule. Clearly state when payments are due and how they should be made.

Forgetting to include consequences for late payments. Outline any fees or penalties to ensure both parties are aware of the terms.

Failing to provide a signature from both the borrower and lender. This is necessary for the document to be legally binding.

Not having a witness or notary present when signing, if required. This can affect the enforceability of the note.

Using vague or unclear language. Be specific to prevent misunderstandings about the terms.

Overlooking the need for copies for all parties involved. Each party should retain a signed copy for their records.

Misconceptions about the New Jersey Promissory Note form can lead to confusion and potential legal issues. Below are seven common misunderstandings:

After gathering the necessary information, you are ready to fill out the New Jersey Promissory Note form. This form requires specific details about the loan agreement between the borrower and the lender. Make sure to have all relevant information on hand to complete it accurately.

Once completed, review the form for accuracy. Both parties should keep a copy for their records. This ensures everyone is aware of the terms agreed upon.

When filling out the New Jersey Promissory Note form, it is essential to follow specific guidelines to ensure the document is valid and enforceable. Here is a list of dos and don'ts to keep in mind:

Texas Promissory Note Requirements - The borrower commits to repay the loan under the agreed terms.

Promissory Notes for Personal Loans - This form serves as proof of a loan agreement between two parties.

For a smooth transaction when selling or buying a vehicle in Florida, it's essential to utilize the Florida Motor Vehicle Bill of Sale form, which can be found at floridaformspdf.com/printable-motor-vehicle-bill-of-sale-form. This document not only details the transaction but also provides important information that will assist in the transfer of ownership and the vehicle registration process.

Promissory Note Template Ohio - Promissory notes can be used for various loans, from personal loans to business financing.

When filling out and using the New Jersey Promissory Note form, it's important to keep a few key points in mind. Here are ten essential takeaways:

By following these guidelines, you can ensure that your promissory note is clear, effective, and legally sound.