Mortgage Statement PDF Template

Mortgage Statement PDF Template

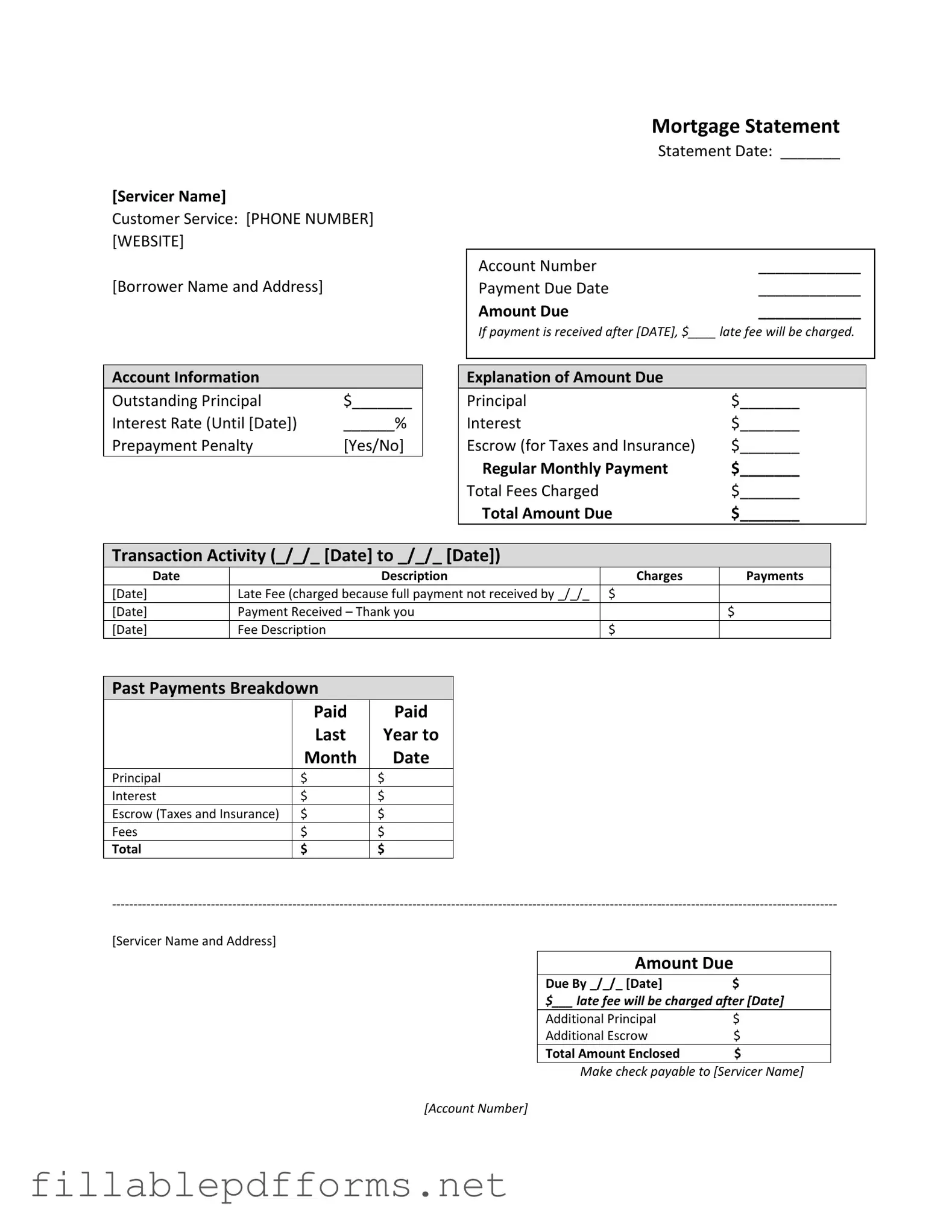

Understanding your mortgage statement is crucial for managing your home loan effectively. This important document provides a comprehensive overview of your mortgage account, including key details such as the servicer's contact information, your account number, and the payment due date. It outlines the amount due, including any late fees that may apply if payments are not received on time. The statement also breaks down the outstanding principal and interest rate, giving you clarity on your financial obligations. Additionally, it highlights any prepayment penalties and provides a detailed explanation of the amounts due, including principal, interest, and escrow for taxes and insurance. You will find a transaction activity section that lists recent charges and payments, along with a past payments breakdown to help you track your payment history. Importantly, the statement contains warnings regarding delinquency and the potential consequences of late payments, underscoring the significance of staying current on your mortgage. If you are facing financial difficulties, the statement offers resources for mortgage counseling and assistance, ensuring you are not alone in navigating these challenges.

Incorrect Account Number: Entering the wrong account number can delay processing. Always double-check this information.

Missing Payment Due Date: Failing to fill in the payment due date can lead to confusion. Ensure this date is clearly indicated.

Omitting Amount Due: Leaving the amount due blank can cause payment issues. Fill this in accurately to avoid complications.

Ignoring Late Fee Information: Not acknowledging the late fee details can result in unexpected charges. Read this section carefully.

Inaccurate Escrow Information: Providing incorrect figures for escrow can lead to problems with taxes and insurance. Verify these amounts before submission.

Partial Payment Misunderstanding: Not understanding how partial payments are handled may lead to frustration. Remember that they do not apply directly to your mortgage.

Neglecting to Sign: Forgetting to sign the form can halt processing. Ensure your signature is included before sending it off.

This is incorrect. Every homeowner receives a mortgage statement, regardless of their payment status. It provides important information about the loan, including payment due dates and account balances.

While the amount due is crucial, additional fees, such as late fees or escrow adjustments, may also apply. Homeowners should review the statement carefully to avoid surprises.

This is not true. Partial payments are typically held in a suspense account and do not count towards the mortgage balance until the full payment is made.

Foreclosure is a lengthy process that usually requires multiple missed payments. Homeowners are often given time to catch up before any drastic actions are taken.

This is misleading. Some loans have adjustable rates that can change after a certain period. Homeowners should check their loan agreement for specific terms.

Not all fees may be listed. Homeowners should inquire about any additional charges that may not appear on the statement, such as servicing fees or insurance costs.

This is a common misunderstanding. The mortgage statement is important year-round for tracking payments and understanding the current status of the loan.

Escrow is often required by lenders to cover property taxes and insurance. Ignoring it can lead to additional fees or complications with the loan.

This is generally not the case. Late fees are typically charged if payments are not received by the due date, regardless of subsequent payments.

Ignoring the mortgage statement can lead to missed information about the loan. Homeowners should regularly review their statements to stay informed about their mortgage status.

Completing the Mortgage Statement form requires careful attention to detail. This form collects essential information regarding your mortgage account, including payment history and amounts due. After filling out the form, you will be prepared to manage your mortgage obligations effectively.

When filling out the Mortgage Statement form, there are several important guidelines to follow. Here are five things you should do and five things you should avoid.

Coat of Arm - Incorporate regional icons to connect with your local heritage.

The Texas Motor Vehicle Power of Attorney form allows an individual to grant another person the authority to manage their motor vehicle-related transactions. This form is particularly useful for those who may be unable to handle these matters personally, ensuring that their vehicle-related needs are addressed seamlessly. For more resources on filling out such forms, you can refer to My PDF Forms, which can provide additional guidance and support.

Car Insurance Templates Free Download - Each driver's information must be documented for insurance claims.

Bill of Ladings - Carriers rely on this document for instructions on how to handle the shipment.

When dealing with your Mortgage Statement form, it's essential to understand its components and how to use it effectively. Here are some key takeaways:

By keeping these points in mind, you can manage your mortgage more effectively and avoid potential pitfalls.