Blank Loan Agreement Template

Blank Loan Agreement Template

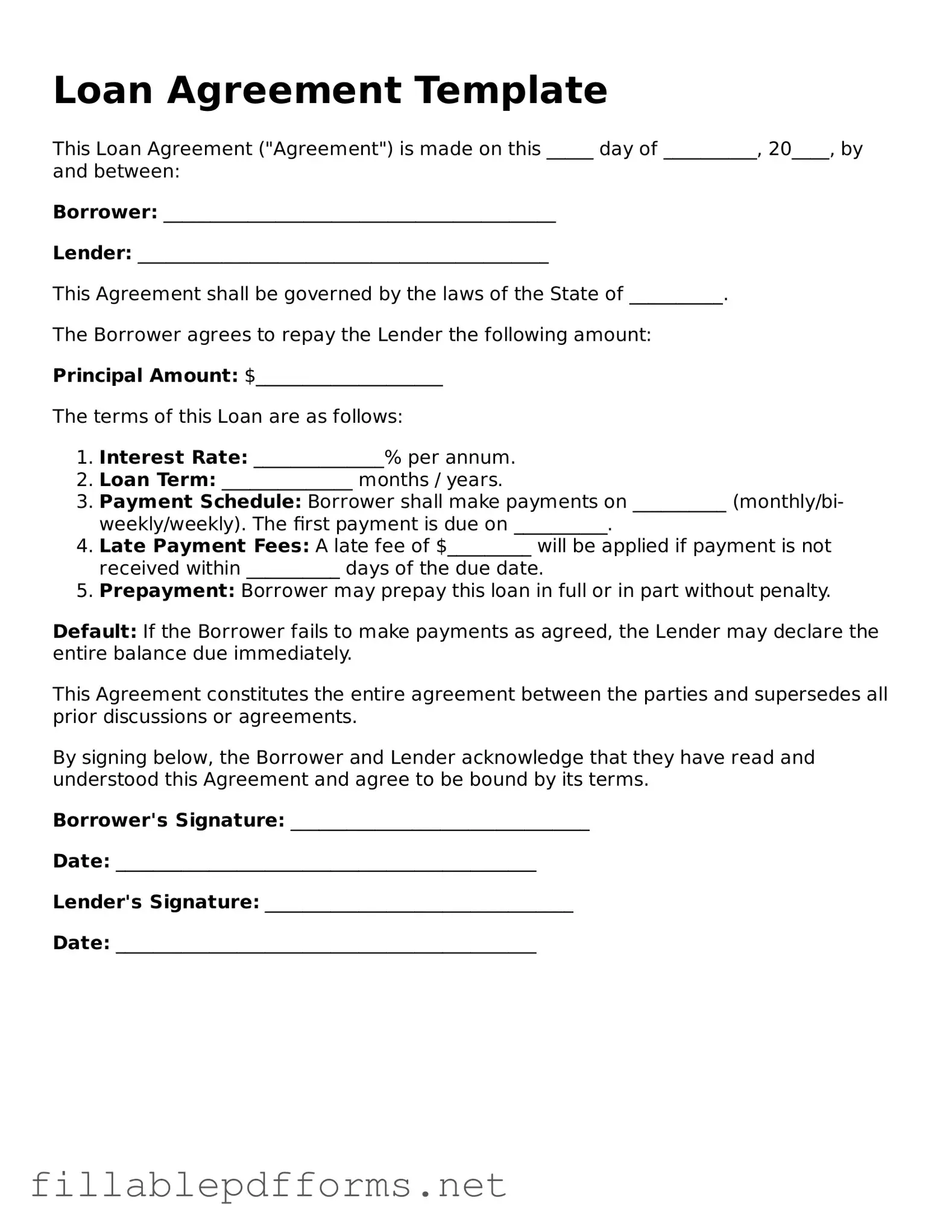

When entering into a loan agreement, clarity and precision are paramount. This essential document outlines the terms and conditions under which a borrower receives funds from a lender. Key aspects of the loan agreement include the loan amount, interest rate, repayment schedule, and any applicable fees. Additionally, it specifies the rights and obligations of both parties, ensuring that expectations are clearly communicated. The agreement also addresses collateral, if applicable, which serves as security for the loan. By detailing these elements, the loan agreement provides a framework that protects both the lender's investment and the borrower's ability to repay. Understanding each component of this form is crucial for anyone looking to navigate the lending process effectively.

Inaccurate Personal Information: One common mistake is providing incorrect personal details, such as your name, address, or Social Security number. This can lead to delays or complications in the loan approval process.

Missing Signatures: Failing to sign the loan agreement can render the document invalid. Ensure that all required signatures are included, both from the borrower and any co-signers.

Ignoring Terms and Conditions: Many people overlook the fine print. It’s crucial to read and understand all terms, including interest rates, repayment schedules, and any fees associated with the loan.

Incorrect Loan Amount: Entering the wrong loan amount is a frequent error. Double-check that the amount you wish to borrow matches what is being requested in the agreement.

Failure to Disclose Financial Information: Not providing complete financial information can hinder the approval process. Be transparent about your income, debts, and other financial obligations.

Not Keeping a Copy: After submitting the form, some individuals forget to keep a copy of the signed agreement. Retaining a copy is essential for your records and for any future reference.

Loan agreements are crucial documents in financial transactions, yet many people harbor misconceptions about them. Below are ten common misunderstandings regarding loan agreements, along with clarifications.

In reality, loan agreements vary widely based on the type of loan, lender policies, and borrower circumstances. Each agreement is tailored to the specific terms negotiated between the parties involved.

The fine print often contains important details about fees, interest rates, and repayment terms. Ignoring it can lead to unexpected costs or obligations.

This is a misconception. Signing a loan agreement creates a legally binding contract. Both parties are expected to adhere to the terms outlined in the document.

While it can be challenging, amendments to a loan agreement are possible. Both parties must agree to any changes and document them formally.

Loan agreements are designed to protect both parties. They outline the rights and responsibilities of the borrower and lender, ensuring fairness in the transaction.

It is essential to read and understand the entire agreement before signing. Knowing what you are agreeing to helps avoid future disputes.

Loan agreements can be used for any amount of money borrowed, whether it’s a small personal loan or a large mortgage. The need for clarity and protection applies regardless of the loan size.

Interest rates can be fixed or variable, depending on the terms agreed upon. It is crucial to clarify this aspect before signing.

Loan agreements are important for all types of loans, including business loans, student loans, and mortgages. Each type of loan requires a clear agreement to outline the terms.

While defaulting can lead to serious consequences, lenders must still follow legal procedures to collect debts. Borrowers have rights that protect them during this process.

Understanding these misconceptions can help individuals navigate the borrowing process more effectively and make informed decisions regarding their financial commitments.

Completing the Loan Agreement form is an important step in securing a loan. This process requires attention to detail and accuracy to ensure that all necessary information is provided. Follow the steps outlined below to fill out the form correctly.

After completing these steps, review the form to ensure all information is accurate. Once satisfied, submit the form according to the lender's instructions.

When filling out a Loan Agreement form, attention to detail is crucial. Here’s a helpful list of things to do and avoid, ensuring a smooth process.

Acord Binder - The form helps to document coverage requirements for employees.

Four Point Inspection Florida - Agents must review the completed form to ensure compliance with all requirements before submitting.

In the realm of real estate, having the right documentation is essential, and the Georgia SOP form plays a pivotal role in this process. Serving as a comprehensive overview of a property's condition, it promotes transparency and helps align the interests of both buyers and sellers. This crucial document not only aids in navigating the complexities of property acquisition but is also important to ensure that all parties make informed decisions. For more information, you can refer to the Georgia Sop form.

Release of Liability Ca Dmv - Participants should not sign without fully understanding the terms laid out in the form.

Filling out a Loan Agreement form is a crucial step in securing a loan. Here are some key takeaways to keep in mind:

Taking these steps seriously can help protect your interests and ensure a smoother loan process.