Gift Letter PDF Template

Gift Letter PDF Template

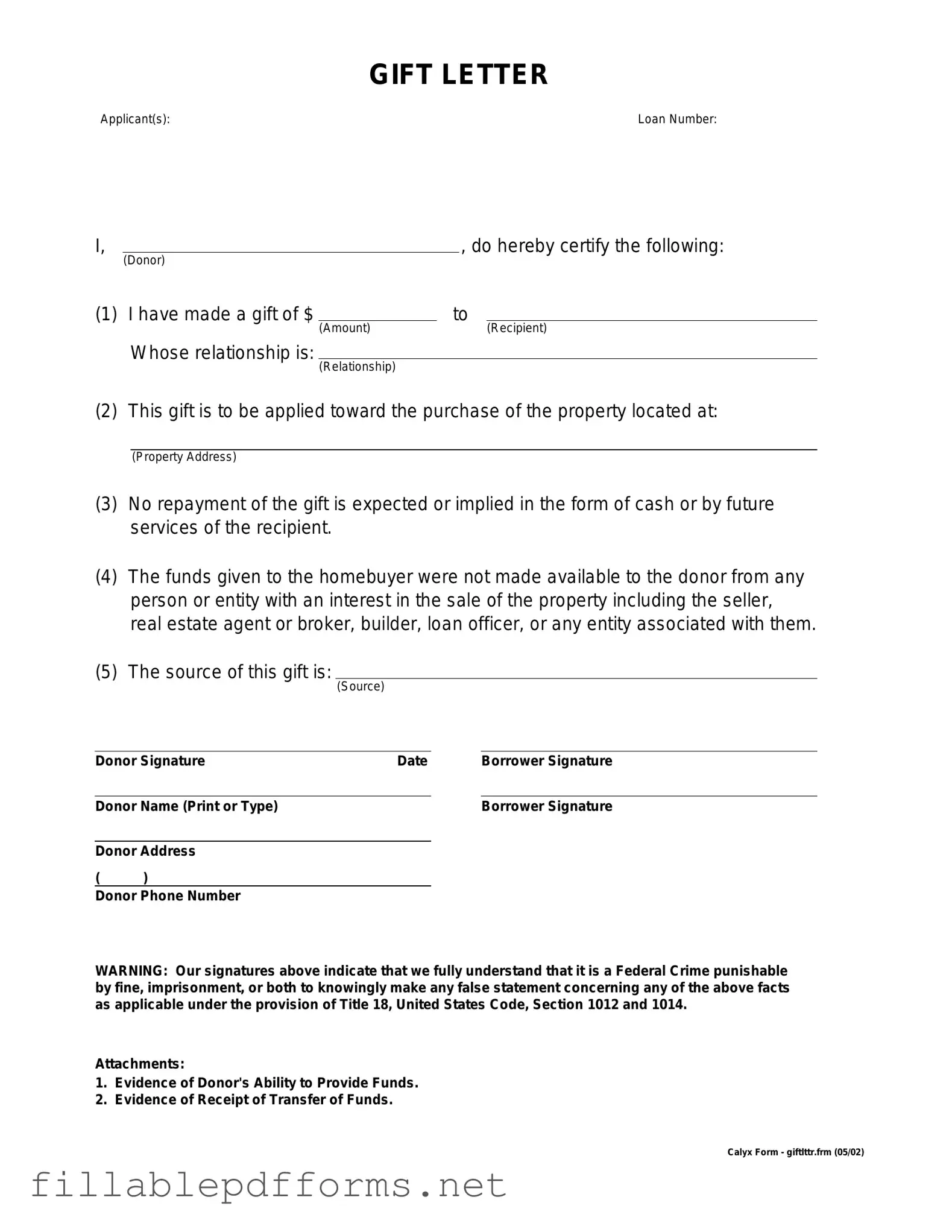

When it comes to securing a mortgage, understanding the Gift Letter form is crucial for both homebuyers and their benefactors. This form serves as a formal declaration that a monetary gift is being provided to assist with the purchase of a home. It outlines key details such as the donor's name, relationship to the buyer, the amount gifted, and a statement confirming that the funds do not need to be repaid. This transparency helps lenders assess the buyer's financial situation more accurately. Additionally, the Gift Letter often requires the donor's signature, adding a layer of authenticity to the transaction. By using this form, all parties involved can ensure clarity and compliance with lending requirements, making the home-buying process smoother and more straightforward.

Inaccurate Information: One of the most common mistakes is providing incorrect details about the donor or recipient. This includes names, addresses, and relationship descriptions. Even a small typo can lead to complications.

Missing Signatures: A gift letter must be signed by both the donor and the recipient. Failing to obtain these signatures can render the document invalid. Always double-check for signatures before submission.

Not Stating the Gift Amount: Clearly specifying the amount of the gift is crucial. Omitting this information can lead to misunderstandings and may raise questions during the loan approval process.

Ignoring the Purpose of the Gift: It's important to explicitly state that the funds are a gift and not a loan. Some people fail to clarify this, which can create confusion for lenders.

Failure to Provide Context: Providing context about the relationship between the donor and recipient can strengthen the validity of the gift. Neglecting to include this information may lead to skepticism from financial institutions.

When it comes to the Gift Letter form, there are several misconceptions that can lead to confusion. Understanding these common misunderstandings can help ensure that the process goes smoothly.

This is not true. Gift Letters can be used by anyone purchasing a home, regardless of whether they are first-time buyers or not. They are simply a way to document that funds received as a down payment are a gift, not a loan.

While many lenders do request a Gift Letter, it is not a universal requirement. Some lenders may have different policies regarding gift funds, so it’s important to check with your specific lender.

Notarization is not always necessary. Most lenders accept a simple signed letter from the donor, provided it includes the necessary information. However, some lenders may have additional requirements, so it’s best to confirm.

Not quite. Typically, lenders prefer that gift funds come from close family members, such as parents, siblings, or grandparents. Some lenders may allow gifts from friends, but this varies by lender.

This is a common myth. The donor does not need to be present at the closing. However, they should be available to provide any necessary documentation if requested by the lender.

This misconception overlooks that gift funds can also be used for closing costs. If the donor specifies that the funds are for closing costs, this should be clearly stated in the Gift Letter.

By addressing these misconceptions, individuals can better navigate the process of using a Gift Letter and ensure that they meet their lender’s requirements effectively.

Filling out a Gift Letter form is an important step in documenting a financial gift. This process ensures that all necessary information is accurately recorded, paving the way for the next steps in your financial transaction.

After completing the Gift Letter form, review it for accuracy. Ensure that all information is correct before submitting it as part of your financial documentation. This will help facilitate the process you are engaged in.

When filling out a Gift Letter form, it's important to follow certain guidelines to ensure the process goes smoothly. Here are four things you should and shouldn't do:

Blank Restraining Order - This order serves as a preventative measure against potential workplace violence.

Hazmat Bill of Lading Pdf - Shippers must abide by mutual agreements regarding property transportation.

For anyone looking to delegate the management of their vehicle-related transactions, the Texas Motor Vehicle Power of Attorney form is an essential tool. By granting this authority, individuals can ensure that even when they are unable to attend to these matters, their needs are handled efficiently. For easy access to this form and additional resources, visit My PDF Forms, which provides all necessary guidance to empower vehicle owners in their decision-making process.

How to Fix Written Mistake on Car Title When Selling - The waiver can serve as a reference for future work or new projects involving the same parties.

When filling out and using a Gift Letter form, several important considerations can help ensure the process goes smoothly. Here are some key takeaways:

By keeping these takeaways in mind, individuals can navigate the Gift Letter form more effectively and avoid potential pitfalls in the gifting process.