Blank Business Bill of Sale Template

Blank Business Bill of Sale Template

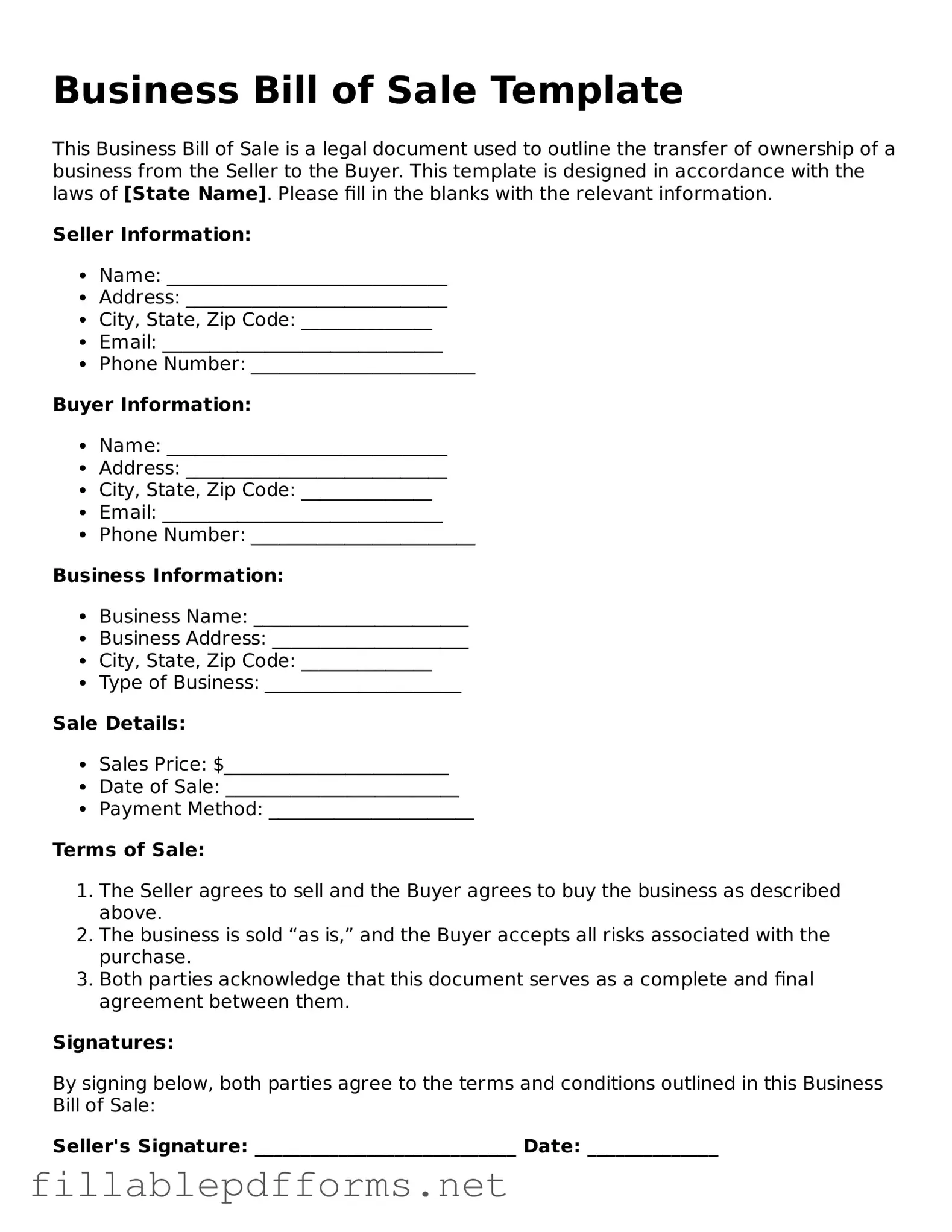

When engaging in the sale of a business, a Business Bill of Sale form serves as a crucial document that formalizes the transaction between the buyer and the seller. This form outlines essential details, including the names and addresses of both parties, a description of the business being sold, and the purchase price agreed upon. Additionally, it may specify any included assets, such as equipment, inventory, or intellectual property, ensuring that both parties have a clear understanding of what is being transferred. The form also provides space for signatures, which solidifies the agreement and indicates that both parties consent to the terms laid out. By using this document, individuals can protect their interests and establish a clear record of the sale, which can be invaluable for future reference or in the event of disputes. Overall, the Business Bill of Sale is not just a piece of paper; it is a vital instrument that facilitates a smooth transition of ownership and helps maintain transparency in business transactions.

Incomplete Information: Failing to provide all necessary details, such as the names of the buyer and seller, can lead to confusion or disputes later. Each party's full legal name should be clearly stated.

Incorrect Date: Entering the wrong date can complicate matters. Ensure that the date of the sale is accurate to avoid any potential legal issues.

Missing Signatures: Both the buyer and seller must sign the document. Omitting a signature could render the bill of sale invalid.

Not Including Payment Details: Clearly stating the payment method and amount is crucial. Vague descriptions can lead to misunderstandings about the terms of the sale.

Neglecting to Describe the Business: A detailed description of the business being sold is essential. This includes its assets, liabilities, and any relevant operational details.

Overlooking Legal Compliance: Not checking local laws and regulations can lead to issues. Each state may have specific requirements for a bill of sale.

Failing to Keep Copies: After filling out the form, both parties should retain copies. This ensures that everyone has access to the same information in the future.

Ignoring Witnesses or Notarization: Depending on the jurisdiction, having a witness or notarizing the document may be necessary. Failing to do so could impact the enforceability of the bill of sale.

Understanding the Business Bill of Sale form is essential for anyone involved in buying or selling a business. However, several misconceptions can lead to confusion. Here is a list of ten common misconceptions:

Addressing these misconceptions can help ensure a smoother transaction process for both buyers and sellers in the business world.

Once you have the Business Bill of Sale form in front of you, it's time to complete it accurately. This document is essential for transferring ownership of a business and ensuring that both parties are protected. Follow these steps to fill out the form correctly.

After completing the form, ensure that both parties keep a copy for their records. This document serves as proof of the transaction and can be crucial for future reference.

When filling out the Business Bill of Sale form, it's important to follow some guidelines to ensure accuracy and completeness. Here’s a helpful list of things you should and shouldn’t do:

Following these tips will help ensure that the transaction goes smoothly and is legally binding.

Private Firearm Bill of Sale - The Bill of Sale empowers buyers by providing them legal documentation of their purchase.

For those looking to create a Texas Bill of Sale form, it is essential to utilize reliable resources that provide accurate templates and guidance. One such resource is My PDF Forms, which offers customizable options to ensure that all necessary information is captured in accordance with legal requirements.

Horse Bill of Sale Form - Provides a framework for any breed registration transfers needed.

When filling out and using the Business Bill of Sale form, keep these key takeaways in mind: